...... Nobody can hope to understand the economic phenomena of any, including the present, epoch, who has not an adequate command of historical facts and an adequate amount of historical sense or of what might be described as historical experience. ........ the historical report cannot be purely economic but must inevitably reflect also "institutional" facts that are not purely economic: therefore it affords the best method for understanding how economic and non-economic facts are related to one another and how the various social sciences should be related to one another. ....... the fact that most of the fundamental errors currently committed in economic analysis are due to lack of historical experience more often than to any other shortcoming of the economist's equipment. History must of course be understood to include fields that have acquired different names as a consequence of specialization, such as prehistoric events and ethnology (anthropology) - Joseph A. Schumpeter, History of Economic Analysis, Elizabeth Boody Schumpeter, ed. (New York: Oxford University Press, 1954), pp. 12-13.

In Sumer, located in the Tigris and Euphrates river region, a unique accounting method was developed using clay tokens in 8000 B.C. The clay tokens were baked into a spherical sort of envelope and used as a promise to a counterparty to deliver a quantity of goods by a certain date. Based on the timeframe imprinted into the envelope vessel and the tokens themselves, sellers promised to deliver the assets. This exchange essentially functioned as a sort of forward contract, which was settled once the seller delivered their goods by the date baked onto the token.

“If any one owe a debt for a loan, and a storm prostrates the grain, or the harvest fail, or the grain does not grow for lack of water; in that year he need not give his creditor any grain, he washes his debt-tablet in water and pays no rent for the year.” - 48th law from the Code of Hammurabi.

Hammurabi, who was the king of Babylon devised a code to ensure that farmers having loans on their houses were not required to pay annual interest in the form of grain in the event of crop failure. In such a scenario, farmers' right not to pay interests is similar to what we now-a-days call put options.

Forward and option contracts on tulip bulbs flourish in Holland. Tulip bulb prices collapse in the winter of 1637,

causing significant contract default.

Options to rent olive presses are described in Aristotle’s Politics.

Chicago Board of Trade (CBT) is formed on April 3, 1848, to provide a centralized marketplace for cash and forward transactions in grains.

CBT revamps forward markets by introducing futures contracts on agricultural commodities. These new contracts were standardized contracts in terms of quality, quantity, time & place of delivery, and involved the use of a clearinghouse and a system of margining.

Chicago Produce Exchange (CPE) is formed to trade futures on butter, eggs, poultry, and other perishable products.

London Corn Trade Association introduces the first futures contract in the United Kingdom.

Coffee Exchange (CE) is formed by a group of coffee merchants to trade futures on coffee.

Butter and egg dealers withdraw from the CPE to form the Chicago Butter and Egg Board (CBEB).

Winnipeg Commodity Exchange (WCE) introduces first commodity (oat) futures contracts in Canada.

Commodity Exchange (COMEX) is formed and introduces the first futures contract on a non-agricultural commodity — silver.

London Metal Exchange (LME) lists the first metal (lead) futures contract in October in the U.K.

Chicago Mercantile Exchange (CME) introduces the first futures contract on livestock - frozen pork bellies.

CME introduces the first futures contract written on a financial instrument, which was on foreign currencies.

CBT organizes the Chicago Board Options Exchange (CBOE) for the purpose of trading call options on 16

New York Stock Exchange (NYSE) common stocks.

CBT introduces first interest rate futures contracts — Government National Mortgage Association (GNMA) futures. In the same year in January American Stock Exchange (AMEX) launches call options on stocks.

CBOE and AMEX listed for the first time put options on common stocks are. CBT also launched Treasury bond futures contracts.

The first over-the-counter (OTC) Treasury bond option takes place.

Interest rate swap transaction takes place for the first time over-the-counter (OTC). CME introduces the Eurodollar futures, which is the first cash settlement futures contract.

The notional amount of OTC derivatives trading surpasses exchange-traded derivatives.

Credit derivative contracts begin trading in the OTC market.

CBOE launches futures contract written on CBOE Market Volatility Index (VIX).

Python: Let's start....

Python: Let's start....![\[\$1,000 \times 0.10 = \$100\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-d699ca4b06f99717a5b59914145183c6_l3.png "Rendered by QuickLaTeX.com")

![\[\$1,000 + \$1,000 \times 0.10 = \$1,000(1+0.10) = \$1,100\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-77e4f7de80480220f592916705e149d4_l3.png "Rendered by QuickLaTeX.com")

![\[\$1,000 + \$1,000 \times 0.10 = \$1,100\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-5d3380331c92426fa5a98b2ab8345376_l3.png "Rendered by QuickLaTeX.com")

![\[\$1,000(1+0.10) = \$1,100\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-2a6b6f00baad85143086ae33ffa3255e_l3.png "Rendered by QuickLaTeX.com")

![\[\$1,100 + \$1,100 \times 0.10 = \$1,210\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-c302f5d162a4507bb70554d2b710c5b1_l3.png "Rendered by QuickLaTeX.com")

![\[\$1,100(1+0.10) = \$1,210\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-2306a916554fd21b51335bef14d84fd6_l3.png "Rendered by QuickLaTeX.com")

![\[\$1,000(1+0.10)(1+0.10) = \$1,210\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-8d8d98c2e0e7c6427b480c215adf6d9f_l3.png "Rendered by QuickLaTeX.com")

![\[\$1,000(1+0.10)^2 = \$1,210\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-eb46078153973466f5e6d3ac9cd43d64_l3.png "Rendered by QuickLaTeX.com")

![\[\$1,210(1+0.10) = \$1,331\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-80c1bf180001dc707bdda1a6f78d0b13_l3.png "Rendered by QuickLaTeX.com")

![\[\$1,000(1+0.10)(1+0.10)(1+0.10) = \$1,331\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-633c9ecdfb4c76bb5baaeecfa0478364_l3.png "Rendered by QuickLaTeX.com")

![\[\$1,000(1+0.10)^3 = \$1,331\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-e55d4a500ff27f77f78c89db56f56132_l3.png "Rendered by QuickLaTeX.com")

![\[\$1,000(1+0.10)^4 = \$1,464.10\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-7034099e0aa894cb43be6070fa64eb32_l3.png "Rendered by QuickLaTeX.com")

![\[\$1,000(1+0.10)^5 = \$1,610.51\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-0c9c00d0afb978d9820cfa1e8cefe558_l3.png "Rendered by QuickLaTeX.com")

![\[(1+0.10) = 1.10\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-8118079a2d8df7f195b11d535b4c6dca_l3.png "Rendered by QuickLaTeX.com")

![\[(1+0.10)^2= 1.21\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-cb93eabd09869d401bb97f28e85a4c35_l3.png "Rendered by QuickLaTeX.com")

![\[(1+0.10)^3= 1.331\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-37770eea14614f358fea9c8a75e79699_l3.png "Rendered by QuickLaTeX.com")

![\[(1+0.10)^4= 1.4641\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-aa8d9e5550af80dcb4581ba1521db018_l3.png "Rendered by QuickLaTeX.com")

![\[(1+0.10)^5= 1.61051\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-0f543ada672d6decc019d3c44949d2e4_l3.png "Rendered by QuickLaTeX.com")

![\[(1+0.10) - 1= 0.10\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-8c45882f4579790ccc0a311b997197ae_l3.png "Rendered by QuickLaTeX.com")

![\[(1+0.10)^2 - 1 = 0.21\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-ad417d2c1659a0ba4d2a177f05904c06_l3.png "Rendered by QuickLaTeX.com")

![\[(1+0.10)^3 - 1 = 0.331\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-5767dca809c56a7830f60be897ec4a7a_l3.png "Rendered by QuickLaTeX.com")

![\[(1+0.10)^4 - 1 = 0.4641\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-b579c809da3b071c7bb73014b16a3215_l3.png "Rendered by QuickLaTeX.com")

![\[(1+0.10)^5 -1 = 0.61051\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-a7cf161d34193e3ee6a346fb1f6ab10d_l3.png "Rendered by QuickLaTeX.com")

![\[\left(1+r\right)^t - 1\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-7efd7306b37db10e4921d3a1be0333e7_l3.png "Rendered by QuickLaTeX.com")

![\[M_t = M_0(1+r)^t\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-bf58e380d3f68bb40507adff9b1834b5_l3.png "Rendered by QuickLaTeX.com")

![\[\left(1+\frac{r}{2}\right)^2\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-ec5b37cd19fdd50bca5fc4d39b4c78a5_l3.png "Rendered by QuickLaTeX.com")

![\[\left(1+\frac{r}{4}\right)^4\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-7ed8106eb961894b5a8c21eb1f8cd2d3_l3.png "Rendered by QuickLaTeX.com")

![\[\left(1+\frac{r}{12}\right)^{12}\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-c45449790fd7a26fed9713a65574fbdc_l3.png "Rendered by QuickLaTeX.com")

![\[\left(1+\frac{r}{52}\right)^{52}\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-6fe5721d034cd8bc5ac30ab8d9a46629_l3.png "Rendered by QuickLaTeX.com")

![\[\left(1+\frac{r}{365}\right)^{365}\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-6f5edaf25c76f81113f026f185fc9f1f_l3.png "Rendered by QuickLaTeX.com")

![\[\left(1+\frac{r}{m}\right)^m\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-5d23a05fc1ba36127a07baaa3010e69c_l3.png "Rendered by QuickLaTeX.com")

![\[\left(1+\frac{r}{m}\right)^{mt}\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-4d82ffe910d84a3ca7a8f0769263a54b_l3.png "Rendered by QuickLaTeX.com")

![\[M_t = M_0 \left(1+\frac{r}{m} \right)^{mt}\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-ae1ed460b8fbc8a66ebea902d6708a1f_l3.png "Rendered by QuickLaTeX.com")

![\[M_t = M_0 \left(1+\frac{r}{m}\right)^{mt}\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-cf75d643ceefde8f8d9e3a0e8fe8215c_l3.png "Rendered by QuickLaTeX.com")

![\[M_2 = 5,000 \left(1+\frac{0.08}{2} \right)^{2\times 3} = 5,000(1+0.04)^6=5000(1.265) = 6,325\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-4c1dfd2cf42435ecc899880e5e7a6667_l3.png "Rendered by QuickLaTeX.com")

![\[M_12 = 5,000 \left(1+\frac{0.08}{12} \right)^{12\times 3} = 5,000\left(1+0.0067\right)^{36}=5000\left(1.272\right)=6,360\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-8eed133e9ff3c3e7c68e57b1411398f4_l3.png "Rendered by QuickLaTeX.com")

![\begin{equation*} e= \lim_{n\to \infty}\left [1+{\frac{1}{n}\right]}^n \end{equation*}](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-c7b276c7dd6c6790ccd3c0095c772f04_l3.png "Rendered by QuickLaTeX.com")

![\begin{equation*} e^r=\sum_{n=0}^{\infty}{\frac{r^n}{n!}}={\frac{1}{0!}}+{\frac{r}{1!}}+{\frac{r^2}{2!}}+{\frac{r^3}{3!}}+\dots= \lim_{n\to \infty}\left [1+{\frac{r}{n}\right]}^n \end{equation*}](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-29751f9dcd22e4474101e3870800dc22_l3.png "Rendered by QuickLaTeX.com")

![\begin{equation*} \lim_{n\to \infty}\left [1+{\frac{0.25}{n}\right]}^n \end{equation*}](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-aeeca399abdc2acd6fe8dcf0e6e84b0f_l3.png "Rendered by QuickLaTeX.com")

![\begin{equation*} e^{r.2}=\lim_{n\to \infty}\left [1+{\frac{r}{n}\right]}^{n.2} \end{equation*}](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-8d121b08771930abc899354899ced01a_l3.png "Rendered by QuickLaTeX.com")

![\begin{equation*} e^{rt}=\lim_{n\to \infty}\left [1+{\frac{r}{n}\right]}^{nt} \end{equation*}](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-891317774ffeda8f23c681d92b3cf4c3_l3.png "Rendered by QuickLaTeX.com")

![\[FV_1 = \$1,000 + \$1,000 \times 0.10 \times 1 = \$1,000(1 + \times 0.10 \times 1) = \$1,100\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-347d9a2059170160eef138b12317e521_l3.png "Rendered by QuickLaTeX.com")

![\[FV_2 = \$1,000 + \$1,000 \times 0.10 \times 2 = \$1,000(1 + 0.10 \times 2) = \$1,200\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-10a388be1aa77c8bb6bcee51f420deee_l3.png "Rendered by QuickLaTeX.com")

![\[FV_5 = \$1,000 + \$1,000 \times 0.10 \times 5 = \$1,000(1 + 0.10 \times 5) = \$1,500\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-364a157f92fb8e191c43f33dba904a36_l3.png "Rendered by QuickLaTeX.com")

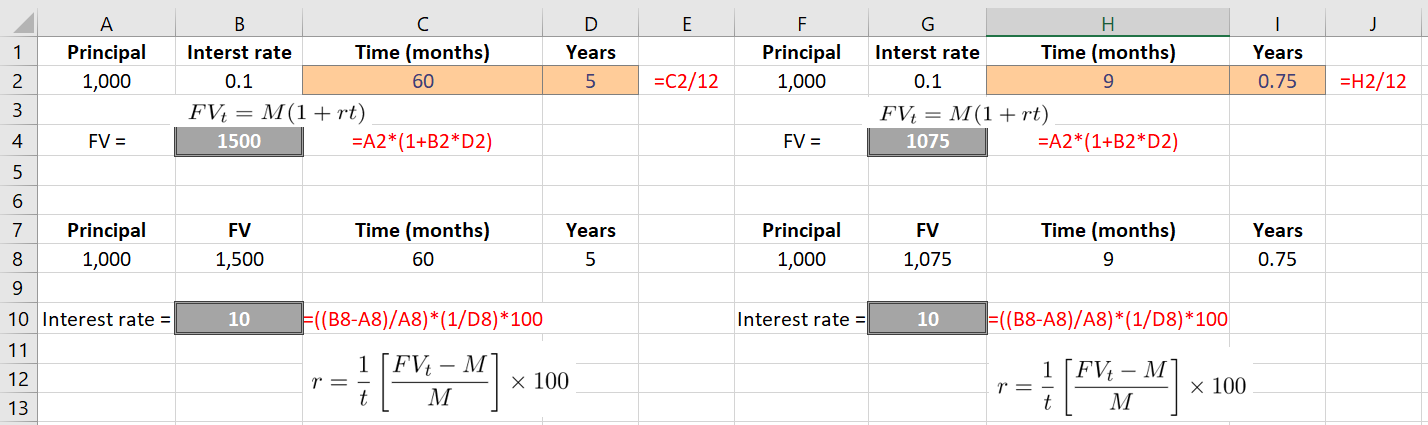

![\[FV_t= M(1+rt)\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-9a01c2a63c5ec014e3012627c66b8f9f_l3.png "Rendered by QuickLaTeX.com")

![\[1+rt = {\frac{FV_t}{M}\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-98f85882b25bb6f6f412d3e4cd7e79b8_l3.png "Rendered by QuickLaTeX.com")

![\[rt = {\frac{FV_t}{M} - 1\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-543921c9a752c0bb3c6408fb8cc7094d_l3.png "Rendered by QuickLaTeX.com")

![\[r = \frac{1}{t}\left [\frac{FV_t}{M} - 1\right]\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-64bd419aebf7e950c8c97607caad81e3_l3.png "Rendered by QuickLaTeX.com")

![\[r = \frac{1}{t}\left [\frac{FV_t-M}{M}\right]\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-4d10f61717d6446bcf6ac701ac58e484_l3.png "Rendered by QuickLaTeX.com")

![\[r = \frac{1}{t}\left [\frac{FV_t-M}{M}\right]\times 100\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-3890ac1d19f7d0fc1d97a0a70b47b239_l3.png "Rendered by QuickLaTeX.com")

![\[\frac{FV_t-M}{M}\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-44d545a6d39b83ad8a6aa28d833b0937_l3.png "Rendered by QuickLaTeX.com")

![\[r = \frac{\text {Total interest}}{M \times t} \times 100\]](https://myriskbook.com/wp-content/ql-cache/quicklatex.com-56d271c10f5450f73de7634c23027461_l3.png "Rendered by QuickLaTeX.com")